Starting at the worst possible time to invest: literally.

When I wrote Part 1 of the $2000 Passive Income Experiment, the stock market was booming along with virtually every other market. Not long after, Part 2 of the $2000 Passive Income Experiment laid out what indexes and companies I am investing in. At that time public sentiment was positive and cash was flowing. Almost immediately afterward, things changed drastically. Global infection rates of COVID-19 became topic of public conversation and a resulting stock sell-off began.

Besides generally being afraid for their own health and wellness along with the health of loved ones, the accompanying sentiment is that people will need to be quarantined and thus, not spending money like they normally do. This of course is true, is happening, and the effects are easily visible in the market. Profits have dropped, valuations have dropped, and general business outlook has dropped.

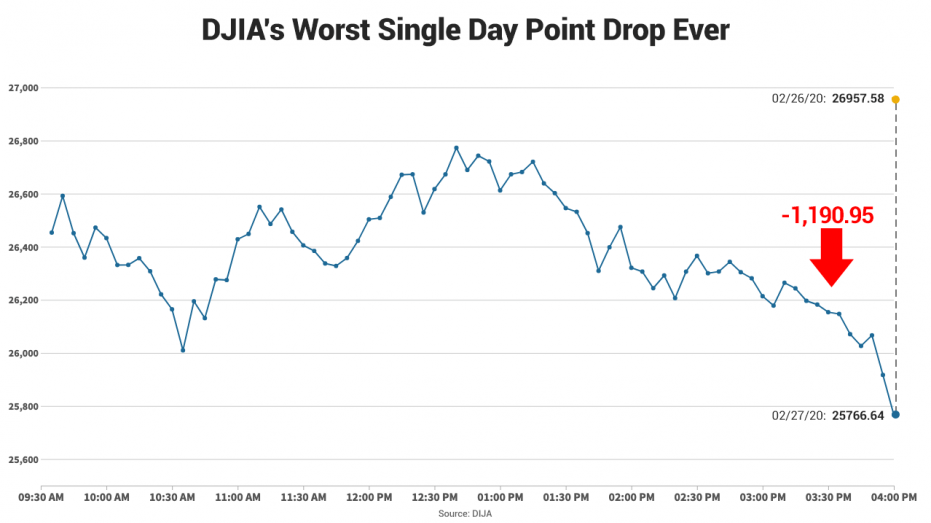

This is not an inappropriate response. As much as I personally dislike the effect it has on everyone’s finances, it makes sense. We are regularly setting of the stock market’s “circuit breaker”. Here’s a breakdown of when that happens via Vanguard’s website:

Level 1 halt (7%)

- Trading will halt for 15 minutes if drop occurs before 3:25 p.m.

- At or after 3:25 p.m.—trading shall continue, unless there is a Level 3 halt.

Level 2 halt (13%)

- Trading will halt for 15 minutes if drop occurs before 3:25 p.m.

- At or after 3:25 p.m.—trading shall continue, unless there is a Level 3 halt.

Level 3 halt (20%)

- At any time during the trading day—trading shall halt for the remainder of the trading day.

We’re responding so quickly to the anticipated future that we actually have to have these speed bumps in place to slow things down. (“We” meaning, humans. Not necessarily me or my community in particular. I like to think of us all in the same boat, especially in light of a pandemic.)

This has meant that the value of all of the dividend investments I chose a couple months ago has plummeted. “But wait”, you may interject, “aren’t these dividend paying companies? Shouldn’t the value of the stock NOT be your primary concern, since they were specifically chosen for their regular dividend distributions?” Why, yes dear reader, you are correct.

It’s been a difficult ride emotionally to see the valuations drop, but the dividend is why we came here in the first place. So, how’s the dividend payout been so far? To put it bluntly, it feels a bit like I’m playing an uneventful game of hide-and-go-seek with dividends. Somehow I thought the game would start earlier. And move quicker. And be more exciting. In general, I’ve only gotten a handful of very small dividends.

First: The individual companies I chose through Robinhood have paid a total of 4 dividends. They are:

- XOM: February 10, dividend of $0.87/share X 2 shares= $1.74 total received

- MMM: February 13, dividend of $1.47/share X 1 share= $1.47 total received

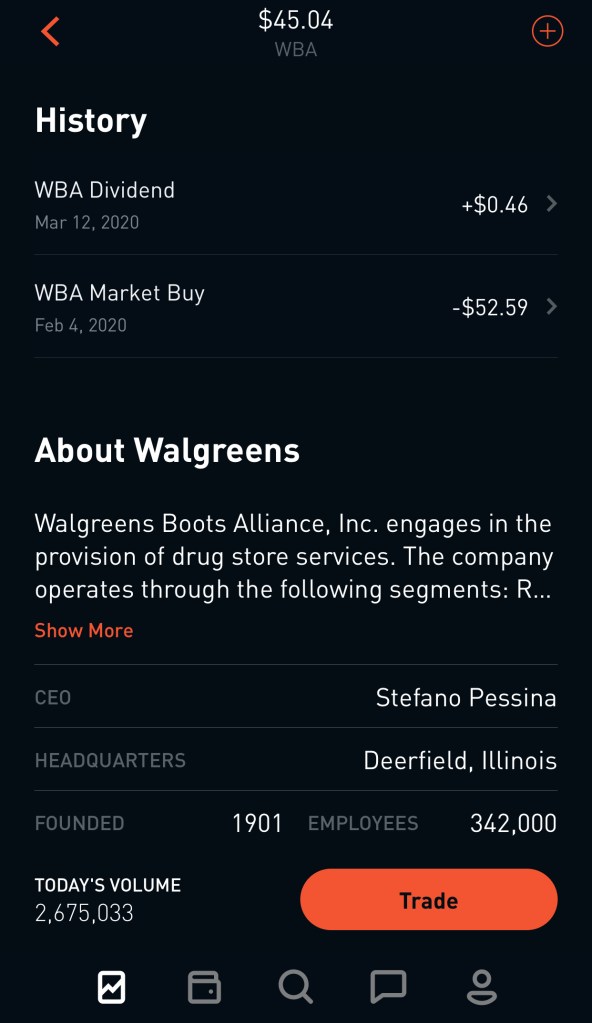

- WBA: February 18, dividend of $0.46/share X 1 share= $0.46 total received

- PSEC: February 27, dividend of $0.06/share X 2 shares= $0.12 total received

- Total= $3.79

- Total dividend return 0.38%

Robinhood continues to be the simplest, easiest, most intuitive investing platform by far. It is very clear what is happening with each investment you choose and when an upcoming dividend is scheduled. Then once the dividend is paid, it is clearly shown on your summary for that particular stock. Here’s what Walgreens looks like when I scroll to to the bottom of the screen:

The dividends paid so far by these companies have been about on track with my expectations. However, the dividends for the rest of this calendar year should be far less than expected. The negative effects of COVID-19 will likely hit profits hard for all of these companies, with the exception of Walgreens. It may actually benefit financially!

Second: Diversified funds chosen to pay dividends through Webull

If you remember from Part 2 of the $2000 Passive Income Experiment, the goal with these investments was to gain significantly more diversity than the ones chosen with Robinhood. These funds hold many different companies, so the rise or fall of a specific stock is not felt as much. My assumption was that this would prove to be the winner in the long run, but with the outbreak of COVID-19, it feels like there won’t be a winner as much as an investment that loses less!

Thus far, no dividends have been paid from these investments! At time of writing technically the end of the first fiscal quarter has not come, so that may be the point at which many companies and funds normally would pay their first dividend of the year. In any case, I’m not planning to sell these investments any time soon so we should have plenty of time to see what happens in the future.

Photo by icon0.com on Pexels.com

Also, Webull isn’t as anxious to tell you everything that happens the moment it happens like Robinhood. They are more “old school” when it comes to updates and changes to your account. One of these areas seems to be dividend payouts. Robinhood makes a push notification appear, shows it on the “Messages” tab, and files it on the page of the stock itself (when you view it on your device). So you can’t really miss it. Webull (I trust!) only shows dividend payouts on the monthly statement after it’s happened.

The roller coaster of volatility in recent days and weeks is one of the reasons why dividend investing seems interesting to me. As long as companies still agree to pay their dividend, the price of the index or stock itself sort of doesn’t matter. Thus far the start of this experiment has been slow, but I anticipate it picking up in the near future!