Hi, I'm Brendan. My goal: help people better understand their money and how to plan a bright future with it. I want everyone to have a secure financial foundation and enough understanding to get there! I'm a 30-something Millenial with a passion for learning and adventure living in the Southwestern United States with my wife and baby.

But does that make it a better investing app? I say no.

Robinhood has a reported 10 million users. That is a lot of people, many of whom likely would not have started investing were it not for the unique approach taken by Robinhood. But the same features that make it seem attractive initially serve to stunt the financial growth of it’s users. In this post I will lay out why I feel this way.

Ease of use

Limitations inherent in this “beauty over substance” approach actually weaken it’s ability to be a useful tool. Lately I’ve been checking the app a lot. This is one problem: ease of checking your daily progress. Or lack thereof these days! It stimulates day trading, i.e. bad decisions for you. The fact that my work-sponsored 401k is a massive pain to login to, check, make any changes, etc… decreases the likelihood that I jump in and make rash (i.e. stupid) decisions in the heat of the moment.

2. Clean design

The clean design looks really nice, but it lacks some of the detail you likely want. I want to know the expense ratio of the funds that may be worth considering. If one is 0.04 and another is 0.3 and they accomplish similar objectives, why would I choose to pay 7.5 times as much! We need to know this! Make this clear app dev people!

3. Daily updates

Daily updates on how your stock is doing via notifications. + Live graphs for the day + Instant deposits + ease of trades + second-by-second updates on your account balance as the market moves + the generally cartoonish nature of the app all push you toward short term thinking. What emphasis is there on buying and holding for the long term as experts recommend? (Not sales people, experts. Your broker may not have your absolute best interests at heart either consciously or unknowingly.)

4. Emphasis on individual stocks

Perhaps most significantly, the emphasis by default design is destined to direct users toward individual stocks! This means that the vast majority of users will have very poorly diversified portfolios. Remember, for now the option of fractional share investing is not available to anyone but the select few people who have been given early access. So I am stuck with a few of this stock and a handful of the other. Perhaps we can force ourselves to wisely branch out and buy a multitude of companies in a sector, but I am partial to believe that most of us probably chose to stick with simply buying more shares in the few companies we started with. This mean we pigeon-hole ourselves into extremely limited diversity and high risk. This design actually ensures that the vast majority of Robinhood investors get WORSE returns than if the emphasis was on low cost index funds. Remember, index funds are available on Robinhood, you just have to search them out.

5. Gamify the process

Also, the game-ifying of the app make it feel less significant. It feels a little more like a cheap app store game about investing than actually risking your literal hard earned dollars. If you’re like me and are a sucker for games, especially pseudo games that involve numbers, something like Cash Management waiting process is a little too intoxicating. For the unfamiliar, Robinhood is starting to dole out a debit card to a limited number of it’s users. When I first started using the service, I was number 1.2MM in line. Every day you’re allow to tap the screen up to 1000 times, which moves you “up in line”. Also, at somewhat random times you may take a massive leap in line, 10,000-40,000 positions in a day. Obviously another incentive they have for this is to allow any new signups that came from your referral link to move you up in line. I’ve not gotten any referrals so the impact of this on your place is unknown to me. This of course entices you to login daily, invite friends, and generally form a habit of visiting that peaceful minty-green app icon every day.

All of this is fine if you’re a bastion of self discipline. Perhaps you’re not like me and you’ve got ice water flowing through your veins. Perhaps you never cheat on a diet or miss a workout. Perhaps you always keep the promises you make to yourself. This whole post could be a list of complaints about an app that is perfectly neutral and I could be completely wrong. BUT. My guess is that you aren’t a Navy Seal with laser focus on whatever you set your mind to and you are subject to the temptations baked into this kind of design. Watching the market sway it’s hips back and forth like the motion of an expert salsa dancer may just hypnotize you into joining in this dangerous dance of daily trading.

Please don’t misinterpret this post as a binary bashing of a beautiful and generally beneficial app and service. These kinds of things aren’t able to be boiled down to “good” and “bad”….most of the time. (There may be some genuinely scammy or otherwise unethical investing apps and services out there that we legitimately need to avoid like the plague….err virus) I still think Robinhood is the path of least resistance to those that are new to investing. HOWEVER, the easiest path is rarely the best when it comes to adult life. It still overlooks many of the fundamental features I have come to believe are foundational for any financial friends to be able to finesse. Again, fractional shares. Yes, yes, they have the feature and are slowly rolling it out to a select number of users. But again, it’s not available to the public so you are more mentally tied to a stock price than an amount of money you’ve committed to investing and its growth or shrinkage based on percentages.

Also, the lack of IRA options is a bit staggering to me. The fact that we are forced to only operate within taxable accounts and are not able to access tax-advantaged accounts is a massive oversight. The average Robinhood user is younger than most of the investing populous as a whole. Likewise, we are prone to be earning less than the average investor and to have a longer time horizon for our investments to grow. Compound interest has been touted as a wonder of the world, and yet here we are being funneled into a short-term, poorly diversified corral of investing.

These reasons are why my favorite investing app is M1 Finance. It corrects all of these wrongs without creating obvious gaps that I miss. Even so, I find myself spending more time on Robinhood because of its ease of use and design features. However, if I had to delete an investing app TODAY and never use it again, sending all of the funds to another service…it would be Tastyworks. But right after that it would be Robinhood!

If you didn’t already know, I have a Youtube channel! Though that is more commonplace than ever, it’s exciting and challenging for me every single day. It’s actually incredible how many people are watching Youtube. Take a guess. How many people do you think are logged in and visit the site each month? 100 million? More. 350 million? More. 800 million? More! The answer: 2 BILLION logged-in users visit Youtube each month. Madness!

I’ve been making videos for just over a year now. A year already! It’s wild how fast the time has flown. While only about 30 videos are publicly viewable, about 2 dozen more are “Unlisted” which means they are only viewable if you have the link. These are mostly family videos. The old days of family holidays, birthdays, get-togethers, and milestones are going by the wayside since everyone just records 30-second clips on their phones. I plan to change that for our family.

The topics have largely been the same as what I’ve written about here on this blog. Exercise, home workouts, motivation, personal finance, investing basics, home buying tips, etc… But unlike the written word, a video is exponentially more difficult to produce. Not only do you need words to say, but you have to deliver them audibly in an engaging way, have a visible image worth looking at, AND edit it all together in some kind of cohesive and interesting fashion! Whew!

The challenge and the required learning has been SO FUN. Don’t get me wrong, my videos still are nearly unwatchable. Ha! My delivery is uncomfortable for me to watch at least. Plus my experimentation with different editing styles and cameras has meant the quality is questionable. BUT they are improving. I am improving. And it’s showing!

Youtube gives anyone who uploads a video access to incredible analytics. I LOVE them. Sometimes I wonder if the analytics are a large portion of my motivation to continue making videos. It’s just amazingly interesting to see how long people stay on a video, where they found you, how many people chose to watch (or not watch) that particular video, what topics people search for, and on and on.

So why make videos? Well it’s not for the acclaim and financial gain! I have 32 subscribers and have made exactly $0.00 from Youtube. In fact, I’m not on track to make money on Youtube ever. At this rate it would be decades before profits were possible. That’s a little painful to write actually. There are a lot of people making a lot of money on the platform. In fact, the number of creators making over $100k/year increased 40% year over year. It seems like a lot of topics are so simple and yet become wildly popular. Why couldn’t I tap into simple yet effective topics?

Well apparently (as most things in life) this is harder than it looks on the surface. Not only is a “decent” video actually INCREDIBLY difficult to make, but then getting the work done before and after the video itself rears it’s time consuming head! The research, set up, preparation, scripting, camera gear setup, and more all takes about 5x longer than I thought it would. I was wrong to assume it would take next to no time, but the reality was still a shock. Then the video is filmed and the real work begins.

After filming/recording, you have to edit. And video editing is literally it’s own craft. One of the unexpected and much appreciated side perks of making these videos has been a newfound appreciation for all things video. Learning about the sheer amount of work, intentionality, preparation, expertise, and effort that goes into major movie productions is absolutely amazing. There are people who are not only video editors for a living, they are even more specialized. Some people are experts in color. “Colorists” are some of the most important people in a production.

The amount of effort that is possible to work into even a 1 minute video is amazing. Or depressing? I don’t know. Because the headroom is almost endless I feel the pressure to spend as much time and energy as possible to attempt to accomplish something like acceptable levels of quality. The pursuit continues, because nothing has really been successful so far.

Why write about it? Well, frankly I want you to read this and know that a more engaging option exists and that you should check it out for yourself. Tell me what’s good or bad about the videos or better yet, save yourself the time and just tell me what you want to see in the future.

Plans for future videos include:

Net vs Gross

Roth IRA basics

Traditional IRA basics

Roth IRA vs Traditional IRA

401k basics

401k vs Roth IRA

401k vs Traditional IRA

“Before you Invest” checklist

How I read 46 books in 2019 in my spare time. For free!

Digital minimalism

Credit card churning

Apple Card review

Goal Setting Masterclass

Basics of Google Sheets

How to build a budget in Google Sheets

$2k Passive Income experiment (ring any bells? Its what most of my blog posts have been about here!)

What to do with your 401k after changing jobs

My personal finance journey

Personal Capital review

M1 Finance Review

Robinhood Review

Ally Bank Review

100 push-ups per day for 30 days

And many more

So, what’s the takeaway? Well, I feel like anyone can and possibly should make a Youtube channel for themselves. But approach it with the perspective of having fun and learning. If it catches on and grows, great! I plan to do just that. Also, trying anything new and outside your comfort zone is a great way to foster growth. Having to speak in front of a camera then show the results to the world has been like another public speaking class for me. It’s wonderful and terrible! I highly recommend it! At the same time I also feel like maybe Youtube is not great for someone to just “try” because it is so incredibly competitive. I heard from another Youtuber that last year 7 million new accounts were made. And that every second 887 videos are uploaded. That is an obscene amount of competition. You almost have to be interested in something incredibly obscure and interesting to stand a chance.

In any case, check out some videos here and leave me a comment to let me know you’re a blog reader!

Every year there is a new trend in human nutrition. Depending on the objective, the swings in prescribed methods of fueling your body can be drastic.

Chocolate is good. Chocolate is bad.

Coffee is good. Coffee is bad.

Alcohol is bad. Alcohol is good.

Fat is bad. Fat is good.

Carbs are bad. Carbs are good.

On and on and on. Turning in circles. It feels like we are lost, without a map, wandering around a landscape of endless options and opinions.

But what is the destination of this journey? General healthiness, right? I mean some of us are wanting slightly different outcomes from our eating practices than others, but largely we just desire a healthy body, at a healthy weight, with a healthy proportion of muscle and fat. Barring any specific dietary needs or restrictions from allergies, medical conditions, or religious purposes, that “SHOULD” narrow things down overall.

This was my logic and still is. And in the setting of the modern, western world the path to take with that destination in mind should be fairly straight. Here’s what it is!

Eat as much “real food” as possible. (I.e. as little commercial processing as possible.)

Eat less sugar

Eat less fried food

Otherwise, moderation.

That’s it!

So how did this perspective come about? Bodybuilding! Yes, seriously. Stick with me here. When I was a freshman in high school, I had an emotionally damaging experience. Nothing objectively horrible, but it shamed me enough to put a chip on my shoulder.

I was forgotten by my coach during a sports award ceremony. Then when my teammates reminded him of this oversight, he hastily called me up to stand with the rest of the team and tried to cobble together a few words about my participation and performance over the past season. The line that was burned into my mind like a branding iron was: “…once his strength develops….”.

This was alluding to a lack of ability on my part and the expectation that developing more strength in the future would improve. Not only is this a potentially damaging comment to make about a young man in front of a room full of peers, coaches, parents, and administrators, but the sport in question was GOLF!

GOLF!

A game that demands very little relative strength! GOLF!

The chip on my shoulder was more like a chunk. I was furious, ashamed, belittled, and determined to make sure that never happened again. Every night before getting in the shower I would do as many push-ups as I could. Then before going to bed I would do dumbbell curls until I couldn’t lift the weight any longer. (Typical teenage boy workouts, ha!)

My sister played basketball for the same high school and during their practices the coach would sometimes bring them into the weight room to workout. Since I depended on her for a ride home after school, I was stuck there but now had occasional access to the weight room. I had no idea what I was doing, but dawdled around and did my best to make my little muscles grow and avoid more shame.

When my sophomore year rolled around and I was allowed to enroll in “Weight Training” as an elective, I jumped all over it. It was a relaxed class atmosphere with very little instruction and oversight compared to a normal class. Our grades only depended on our 1-rep max weight increasing over the course of the semester. How we got there and spent the time between “tests” was entirely up to us. I devoured the little information our teacher provided and supplemented it with grocery store muscle magazines.

“How to increase your bench press.”

“How to grow your arms.”

“How to get giant quads.”

“How to build your lats.”

All of the information was flooding into my brain and I was absorbing it all like a thirsty sponge. The next 2 years of high school also included Weight Training class and I was as diligent as anyone in the school with my training. Chest workouts one day. Leg workouts another. An entire day dedicated to arms (of course). Another day spent learning to power clean with better form. And on and on.

The muscle did slowly accumulate over my lanky frame. When the comment was made during that sports award ceremony I didn’t think my strength was lacking. Apparently I was wrong. Now that I had been training for over 3 years, I was much stronger and yet still somehow fully convinced that the deficiency remained. The deficiency that likely wasn’t even there to begin with.

I was 6’4″ tall, weighing a lean 194 lbs despite eating nearly everything in sight. Between weight training, varsity soccer, and varsity track, my body was burning calories at an absurd rate. My 1-rep maxes were deep into “respectable” territory for an 18 year old amateur. I could bench 235, squat 335, and clean 255. Enough to put me toward the top of the class overall. I ran a 4.65 40-yard dash over and over, which was the fastest in the entire school. I was the fastest sprinter on the track team and went on to win the boys 4A State Track and Field title in the 200m, setting a new school record. I also helped to set school records in the 4x100m and 4x400m relays. On top of that, my classmates voted me as “Best Physique” in the senior class, which was immortalized in the yearbook.

Every indicator of success was mine. The story had been overturned. I had irrefutable proof that I was strong enough, fast enough, GOOD ENOUGH. But possibly the last person still holding onto that old belief that my strength had yet to develop was me. That my worth was yet to develop. That adequate reason to remember me was not present. The chip on my shoulder remained.

Once into college my working out intensified. The new environment of a college campus and all of the new people to make a first impression on stoked the fire of my insecurity. I worked out every weekday for between 2 and 4 hours. Heavy weight training, arduous ab workouts, outdoor sprints, and everything in between filled my afternoon schedules.

I was a regular at a nearby community college and befriended an exercise science professor who also worked in their fitness center part time. In fact the fitness center staff was entirely made up of faculty. It was an amazing wealth of knowledge and experience and was the single biggest factor shaping my training, diet, and recovery both then and now. My results continued to accumulate and my sense of self worth continued to…not continue. It stagnated.

Part of my drive to be exceptional physically was to adopt the dietary habits needed to foster the results I was seeking. Obviously a lot of the advertising in the fitness industry is paid for by supplement companies. But man cannot live on protein shakes alone. Or on just chicken, brown rice and broccoli. I needed to foster fat loss, muscle gain, and peak performance without a mentally taxing list of restrictions or a fancy meal plan.

Out of that mentally unhealthy time came a simple and easy to follow guideline for eating. I hate the word “diet” and its connotations so we will avoid it. Guidelines are something you choose with a sober mind and follow because they result in logical and sustainable outcomes. The guidelines at that time were:

No sugar

No fried foods. (except tortilla chips, which are impossible to refuse)

Eat lots of protein

That’s it. Still a good guideline system overall in my opinion, but not as sustainable or as balanced as the 4-Steps above. Notice the change here to completely abstaining from both sugar and fried foods. This along with my propensity for treating workouts like a part time job lead to a ridiculously low body fat percentage of about 4%. They tested it there at that professor-rich community college and I was advised to stop losing body fat because I was at the limit of what is healthy to maintain. Any less body fat and I would be taking steps in the wrong direction. I ate so little sugar that when I visited the dentist they said, “Wow! What do you eat?”. There was so much less decay happening in my teeth than their average patient that it was immediately noticeable.

But abstaining from a whole chunk of available foods is really difficult in the long-term. A little birthday cake or a chicken biscuit won’t throw off your training, progress, or healthy to any measurable degree. So we will switch from “No” to “Less”.

Eat as much “real food” as possible. (I.e. as little commercial processing as possible.)

This guideline came about in 2020 (this year) when I was looking for a single rule I could consider when choosing what to put in my stomach. A simple thought to run through your mind that considers your overall health without the oppression of other voices that are largely driven by shame, guilt, or other damaging motivations. The chip on my shoulder should not be allowed to dictate my life any more.

Eat less sugar

This is probably predictable. But it’s still true. Sugar seems to be in everything that is fast and tasty. Its negative effects are largely known and are commonly understood. It’s still something that is very tempting and very easy to go ahead and give in to. A little flavored coffee creamer, one of those good pastries, a bit of candy before lunch, a fruit smoothie, a little treat in the afternoon, and a scoop of ice cream for dessert is not an uncommon day of dietary indulgences. But if you add up the total amount of unnecessary sugar intake from those little delicious treats, it is ridiculous.

Eat less fried food

Frying food makes it more delicious. One of the universal truths. However, the salty fatty crispy coating also makes it detrimental to your health. Probably. Much of the time I find the food that is being fried is actually so lacking in nutrition or desirability that it’s only through frying that it is able to hold any appeal. Mm-mm potato strips. Not very tasty. French fries: delicious.

Otherwise, moderation.

Always a good idea to take things in moderation. Even if something seems to be really healthy, consuming an obscene quantity can cause detrimental effects. We aren’t made to only consume fruits or only consume meats or whatever the suggested monochromatic trend prescribes. Odds are we need to consume a different ratio of veggies, fruits, carbs, and meats than we currently do, but even then having some of each is likely the healthiest overall choice. Obviously moderating the amount of blatantly unhealthy foods and drinks is wise. But that is often the hardest category in which to exercise self discipline. If a bite of pie is good, then 3 pieces of pie is really good!

One of the most immediately successful habits I have experimented with in my own pursuit of self control and moderation is speed. Just slowing down to consider what is happening can snap you back into reality. Labeling the activity helps bring to light the goodness of the situation and can bring some clarity. “I am in my own home, with people I care about, getting to eat this delicious food. How amazing is this! What a treat! I GET to have this dinner, this dessert, this snazzy cocktail. Wow, this is a privilege.” It is when I am most mindless and emotional that my indulgences run wild and I finish that bag of chips or that pint of ice cream.

Getting results is fun. Getting to the goal weight/size/performance/aesthetic is an achievement for sure. But sacrificing your sense of self worth or sanity is NOT WORTH IT.

-Brendan

Getting results is fun. Getting to the goal weight/size/performance/aesthetic is an achievement for sure. But sacrificing your sense of self worth or sanity is NOT WORTH IT.

The toll this takes on your mental and spiritual health isn’t covered by any physical satisfaction gained along the way. You have to be a whole person. Satisfied, sane, and safe. Telling yourself you aren’t enough, aren’t ok, aren’t who you need to be and letting that be a non-stop recording in your own head is not the way.

The chip on my shoulder has mostly healed. I’m not sure it can ever fully heal. But today, I want to be healthy so I can experience life fully. I can indulge in a brisk run when the weather is good and enjoy the speed my legs still have. I can chase my nieces around for an hour without getting so tired I have to quit. I can help people near me who are not as strong to move heavy things. (This sounds simple and silly, but it actually is a regular occurrence!)

I can have fun setting a fitness goal and working towards it for the thrill of the chase, the development of discipline, and the fun of sharing the journey, without it determining my self worth.

This is the kind of structure we need around our food intake. One that takes into account the bigger goals in life and is both motivating and simple enough to be something we can do for years or decades to come. One that we can talk openly about without feeling ashamed. One that encourages all forms of health, and doesn’t trade physical health for mental health.

Starting at the worst possible time to invest: literally.

When I wrote Part 1 of the $2000 Passive Income Experiment, the stock market was booming along with virtually every other market. Not long after, Part 2 of the $2000 Passive Income Experiment laid out what indexes and companies I am investing in. At that time public sentiment was positive and cash was flowing. Almost immediately afterward, things changed drastically. Global infection rates of COVID-19 became topic of public conversation and a resulting stock sell-off began.

SARS-CoV-2

Besides generally being afraid for their own health and wellness along with the health of loved ones, the accompanying sentiment is that people will need to be quarantined and thus, not spending money like they normally do. This of course is true, is happening, and the effects are easily visible in the market. Profits have dropped, valuations have dropped, and general business outlook has dropped.

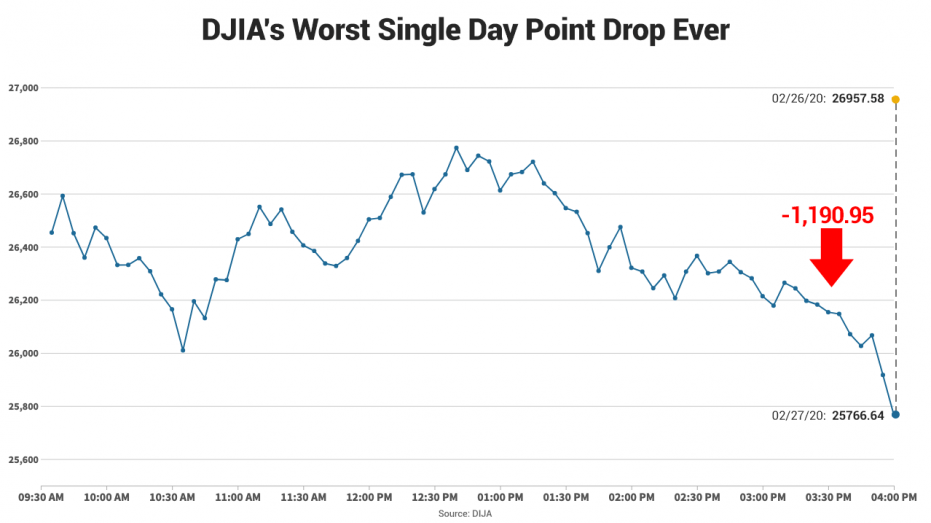

This is not an inappropriate response. As much as I personally dislike the effect it has on everyone’s finances, it makes sense. We are regularly setting of the stock market’s “circuit breaker”. Here’s a breakdown of when that happens via Vanguard’s website:

Level 1 halt (7%)

Trading will halt for 15 minutes if drop occurs before 3:25 p.m.

At or after 3:25 p.m.—trading shall continue, unless there is a Level 3 halt.

Level 2 halt (13%)

Trading will halt for 15 minutes if drop occurs before 3:25 p.m.

At or after 3:25 p.m.—trading shall continue, unless there is a Level 3 halt.

Level 3 halt (20%)

At any time during the trading day—trading shall halt for the remainder of the trading day.

We’re responding so quickly to the anticipated future that we actually have to have these speed bumps in place to slow things down. (“We” meaning, humans. Not necessarily me or my community in particular. I like to think of us all in the same boat, especially in light of a pandemic.)

This has meant that the value of all of the dividend investments I chose a couple months ago has plummeted. “But wait”, you may interject, “aren’t these dividend paying companies? Shouldn’t the value of the stock NOT be your primary concern, since they were specifically chosen for their regular dividend distributions?” Why, yes dear reader, you are correct.

It’s been a difficult ride emotionally to see the valuations drop, but the dividend is why we came here in the first place. So, how’s the dividend payout been so far? To put it bluntly, it feels a bit like I’m playing an uneventful game of hide-and-go-seek with dividends. Somehow I thought the game would start earlier. And move quicker. And be more exciting. In general, I’ve only gotten a handful of very small dividends.

First: The individual companies I chose through Robinhood have paid a total of 4 dividends. They are:

XOM: February 10, dividend of $0.87/share X 2 shares= $1.74 total received

MMM: February 13, dividend of $1.47/share X 1 share= $1.47 total received

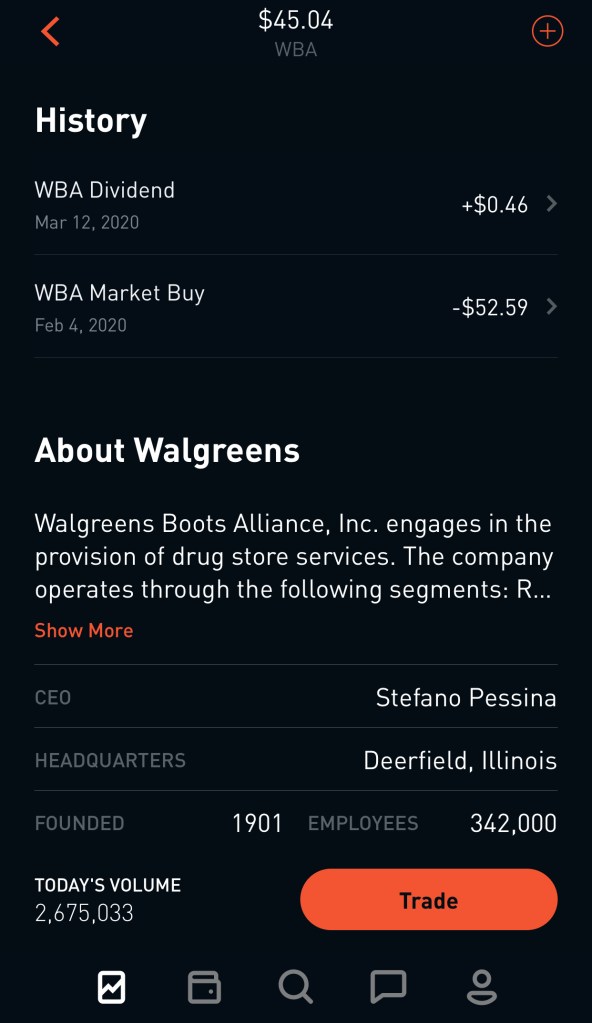

WBA: February 18, dividend of $0.46/share X 1 share= $0.46 total received

PSEC: February 27, dividend of $0.06/share X 2 shares= $0.12 total received

Total= $3.79

Total dividend return 0.38%

Robinhood continues to be the simplest, easiest, most intuitive investing platform by far. It is very clear what is happening with each investment you choose and when an upcoming dividend is scheduled. Then once the dividend is paid, it is clearly shown on your summary for that particular stock. Here’s what Walgreens looks like when I scroll to to the bottom of the screen:

Robinhood app clearly showing dividend amount and date.

The dividends paid so far by these companies have been about on track with my expectations. However, the dividends for the rest of this calendar year should be far less than expected. The negative effects of COVID-19 will likely hit profits hard for all of these companies, with the exception of Walgreens. It may actually benefit financially!

Second: Diversified funds chosen to pay dividends through Webull

If you remember from Part 2 of the $2000 Passive Income Experiment, the goal with these investments was to gain significantly more diversity than the ones chosen with Robinhood. These funds hold many different companies, so the rise or fall of a specific stock is not felt as much. My assumption was that this would prove to be the winner in the long run, but with the outbreak of COVID-19, it feels like there won’t be a winner as much as an investment that loses less!

Thus far, no dividends have been paid from these investments! At time of writing technically the end of the first fiscal quarter has not come, so that may be the point at which many companies and funds normally would pay their first dividend of the year. In any case, I’m not planning to sell these investments any time soon so we should have plenty of time to see what happens in the future.

The dry, empty status of my indexes dividends Photo by icon0.com on Pexels.com

Also, Webull isn’t as anxious to tell you everything that happens the moment it happens like Robinhood. They are more “old school” when it comes to updates and changes to your account. One of these areas seems to be dividend payouts. Robinhood makes a push notification appear, shows it on the “Messages” tab, and files it on the page of the stock itself (when you view it on your device). So you can’t really miss it. Webull (I trust!) only shows dividend payouts on the monthly statement after it’s happened.

The roller coaster of volatility in recent days and weeks is one of the reasons why dividend investing seems interesting to me. As long as companies still agree to pay their dividend, the price of the index or stock itself sort of doesn’t matter. Thus far the start of this experiment has been slow, but I anticipate it picking up in the near future!

But, Mousie, thou art no thy lane [you aren’t alone] In proving foresight may be vain: The best laid schemes o’ mice an’ men Gang aft a-gley, [often go awry] An’ lea’e us nought but grief an’ pain, For promised joy.

-Robert Burns’ poem, To A Mouse, 1786

When starting this experiment I hadn’t even considered the possibility of a stock market correction on the scale of 35%+. Honestly it was a mix of foolish optimism and a lack of experience. For my entire investing lifetime it’s been a bull market. Before 2009 I didn’t have money to invest anyway. Everything was immediately spent! Now that I’m allegedly older and wiser, a significant portion of our combined income goes to investments but I have to admit that this downturn has been an emotional workout!

Enough gloom and doom! Let’s get back to the real content of the experiment at hand!

In this post I’ll outline the specific stocks and funds I chose, why I chose them, and what I anticipate the outcome to be overall.

First: Dividend-paying indexes

Our first group contender is the $1000 invested with Webull into dividend-paying indexes. If you’re not familiar with the concept of an index, here’s a very short explanation. An index is just a group of stocks chosen based on whatever parameters people want, all grouped together into one basket. You buy a portion of the entire basket, getting the benefits of diversifying with all those stocks inside it.

Still feel a little confused? Me too….let’s think about it in terms of pizza!

Photographer Victor Protasio, Food Stylist Rishon Hanners, Prop Stylist Sarah Elizabeth Cleveland

The ingredients of the pizza represent stocks. Flour, water, salt, pepperoni, sausage, tomato, oregano, cheese, olives, onion, etc…. Choosing individual stocks is like just buying the cheese or the salt or a little piece of sausage. If they are really awesome (i.e. increase in value/pay regular dividends) then maybe you’d be happy with just eating them alone. But if you want all of them combined, you would have to go out and buy specific amounts of each to aggregate yourself. That’s a lot of work to find what you want, how much of it you want, and buying it all in pieces.

In contrast, an index is just buying the whole pizza. Its assembled for you with all the right ingredients based on what you ordered. Ah you like the pizza based on the S&P 500? Here you go. Only want the dividends and don’t care about growth, there’s a pizza (index) for you. Whatever your flavor, there’s an index already hot and ready and waiting.

The benefits are that an index is simple, automatically diverse, and readily available. It’s a powerful tool that you can take advantage of now and don’t even need to hire a fancy high-powered financial guru to manage.

“By periodically investing in an index fund, for example, the know-nothing investor can actually outperform most investment professionals. Paradoxically, when ‘dumb’ money acknowledges its limitations, it ceases to be dumb.”

(Warren Buffet, 1993)

I chose a small handful of indexes that are made to follow dividend paying companies. This way I get to take advantage of all of them simultaneously! Here they are:

VIG: Vanguard Dividend Appreciation ETF

VYM: Vanguard High Dividend Yield ETF

JDIV: JPMorgan U.S. Dividend ETF

VIG: Vanguard Dividend Appreciation ETF

Vanguard has always been a go-to investment group for people looking for low fees and great returns. They LITERALLY invented the index fund for this purpose. VIG is a fund that is designed to track another index called the NASDAQ US Dividend Achievers Select Index. That index chooses investments with at least ten consecutive years of increasing annual regular dividend payments. Sounds good to me! On top of that, the expense ratio is a teeny tiny 0.06%! That’s about as close to totally free investing as we are going to get! It holds 186 different stocks and most of them are big names you’ve definitely heard of. Like these:

Month-end 10 largest holdings (35.50% of total net assets) as of 02/29/2020

1

Microsoft Corp.

2

Visa Inc.

3

Procter & Gamble Co.

4

Walmart Inc.

5

Johnson & Johnson

6

Comcast Corp.

7

McDonald’s Corp.

8

Abbott Laboratories

9

Medtronic plc

10

Costco Wholesale Corp.

Sector

Basic Materials

3.6%

Consumer Goods

10.6%

Consumer Services

20%

Financials

11.5%

Health Care

11.9%

Industrials

26.2%

Technology

9.9%

Utilities

6.3%

JDIV: JP Morgan U.S. Dividend ETF

I only chose this ETF because I needed to round out the $1000 total and the price was just about right to do that! I did almost no research to choose it besides noticing the famous name (JP Morgan) and the fact that it held over 200 companies. It turns out that it’s a very small ETF with only about $34 million in holdings. Thankfully, it’s well-diversified over a number of sectors and companies! It is also inexpensive to own with a net expense ratio of 0.12%! That means they only charge you $1.20 for every $1000 invested.

JDIV Top 10 Holdings

As of 03/25/2020

Symbol

Name

Security Identifier

% of Net Assets

Market Value

CLX

CLOROX CO/THE COMMON

189054109

0.84%

216,351.96

GILD

GILEAD SCIENCES INC

375558103

0.82%

211,836.06

DLR

DIGITAL REALTY TRUST INC

253868103

0.82%

210,802.48

CY

CYPRESS SEMICONDUCTOR

232806109

0.80%

206,885.00

LLY

ELI LILLY & CO COMMON

532457108

0.80%

205,346.96

AMGN

AMGEN INC COMMON STOCK

031162100

0.79%

202,410.72

INTC

INTEL CORP COMMON STOCK

458140100

0.78%

201,861.88

VZ

VERIZON COMMUNICATIONS

92343V104

0.78%

200,209.46

JNJ

JOHNSON & COMMON

478160104

0.77%

199,278.60

GIS

GENERAL MILLS INC COMMON

370334104

0.77%

197,271.00

Sector Exposure

As of 03/25/2020

Sector

FUND

Basic Materials

9.5%

Consumer Goods

15.1%

Consumer Services

7.9%

Financials

16.4%

Health Care

7.6%

Industrials

9.5%

Oil & Gas

5.5%

Other

0.0%

Technology

6.4%

Telecommunications

3.7%

Utilities

18.9%

VYM: Vanguard High Dividend Yield ETF

VYM is yet another index that’s made to track some other index. It is designed to track the FTSE High Dividend Yield Index. Unlike the FTSE index it is made up of domestic stocks, but holds a very similar ethos of only holding dividend-paying companies. Like the others, it’s made up of many different companies so all of your eggs aren’t trusting the same proverbial basket. For example, at the end of February the top holding was a tie between JPMorgan Chase & Co and Johnson & Johnson at 3.80%. So even if Chase absolutely plummeted, it’s less than 4% of the whole. The 10 largest holdings in the index make up less than 27% of the total, which gives you an idea of how small each piece of the pie really is. I view this as a good thing. Yes, it’s less likely to have a rocket ship company make me a millionaire overnight, but that also means it’s likely to handle the market downturns better as well.

If you care to compare, there’s the break-down of the different sectors of companies in this index fund:

Portfolio composition

Equity sector diversification

Sector

High Dividend Yield ETF as of 02/29/2020

FTSE High Dividend Yield Index (Benchmark) as of 02/29/2020

Basic Materials

3.30%

3.30%

Consumer Goods

14.40%

14.40%

Consumer Services

9.20%

9.10%

Financials

18.30%

18.30%

Healthcare

14.10%

14.10%

Industrials

8.30%

8.30%

Oil & Gas

7.10%

7.20%

Technology

10.60%

10.50%

Telecommunications

5.20%

5.20%

Utilities

9.50%

9.60%

Whew! Lots of numbers. Just a few more: About 98% of this part of the investments are in the 2 Vanguard funds, with a tiny bit of that oddball JDIV bringing up the last 2%. The point of this exercise is to test how easy it is to just pick 1-2 (or in my case 3 just to round out an even $1k) indexes and “set it and forget it”.

Second: Picking specific companies that pay dividends.

This is what it feels like to me when anyone picks an individual company. Or even a handful of individual companies. I’m FAR from a financial analysis guru, but even people who make a successful career from analyzing companies financial standing can’t accurately and reliably pick winners. The fact that the pro’s lose to “the market” as a whole over 95% of the time makes me realize how small of a chance I actually have to do that kind of thing.

For the purposes of this experiment I picked dividend paying companies that the Interwebs claim are worth considering. Once you type things like “dividend stocks” and “passive dividend investing” into Google, you get a lot of very direct advise (and a lot of people wanting to sell you their opinion) on where to invest your hard earned money.

A lot of people claim the “Dividend Aristocrats” are a sure-fire way to succeed. So I considered those. Others have hot picks based on the current state of the market, of consumer sentiment, of perceived demand, or any other number of factors. Knowing that the pros don’t generally taste success with a TON of smart analysis made me feel like I was partially off the hook when it came to pouring over prospectus statements and P/E ratios and all the other paperwork available. I went with what made sense at the time and didn’t look back.

SO, who did I choose. These lovely companies:

F: Ford

ABBV: AbbVie

AOS: A.O. Smith

MMM: 3M

PBCT: People’s United Bank

WBA: Walgreens

XOM: Exxon Mobile

T: AT&T

PSEC: Prospect Capital

The only company that I didn’t choose strictly on the recommendations of logic and anonymous internet brethren was Ford. I like their vehicles. I’ve also wanted to invest in them since 2010, and have regretted not since at the time the stock was only $2.00/share. It’s risen a lot since then and has paid dividends along the way.

You’ve likely heard of a handful of these companies and have an idea of what they do. I’d never heard of PBCT or PSEC. People’s United Bank is a bank and financial holding company doing….bank sounding stuff. (Insert shrug emoji here!) And Prospect Capital is a business development company that basically lends money to companies or invests in them directly. Anyway, enough about them.

In next week’s post I’ll share how the results have fared thus far. Fair warning: it is NOT pretty.

Titles we inevitably work very hard to earn. To legitimize. This is no easy badge to wear. We likely have invested hundreds of hours in our activity of choice to become known as and feel worthy of a title like these. We have achieved a level of mastery above many of our peers or coworkers. We have seen results in our bodies and minds and now trust that the activity is a worthwhile expenditure of our limited resources.

It’s probable you have begun to self-identify as one of the names above. However, the best form of a fitnessy-label comes from the outside. Someone else calls you a Yogi, so you must be one. It’s THAT evident. Or you spend 2 hours per day in a dark weight room, lifting as heavy as you can, wearing your hoodie and taking swigs of the latest fizzy pre-workout beverage. Someone at work happens to notice your arms seem bigger than before and, “You must work out” is given as the justification for the change. Boom. Verified weightlifter/bodybuilder. Everyone can see the product of your labor right in front of them, bulging out from under those puny sleeves, helpless against the power of your blooming new triceps.

But the final confirmation is the sweetest. This is when a member of the elite labels you as one of their own. The woman with the most poise and grace in the whole class calls you a great dancer. The climber who flashes 5.13’s comments that your beta is infallible. The coach says your improvement with thrusters is the best he’s seen all year from anyone and maybe you should help bring beginners up to speed. Someone with the power to induct you into the marbled halls of the elite has claimed you belong.

Like a variation of ancient coming-of-age traditions, you’ve made it. You killed the lion, drank the cow’s blood, wore the gloves full of bullet ants, and are given this identity.

Accept it with caution.

Yes, you have focused your efforts and resources. Yes, you have realized results. Yes, you have been recognized by a community as a valid participant. But are these positives? These are not objectively negative things. However, assuming an identity based on them is something to handle with great caution. The problem I have with weaving your identity into the activity you enjoy is that it’s a petty representation of who you are. As a person, you are a citizen, a family member, an employee (possibly an employer), a friend, a human. Your depth and beauty and power are vast. Almost incomprehensible.

If your identity is decided by your actions, your worth is measured by your results.

Read that again, and slow down. “If your identity is decided by your actions, your worth is measured by your results.” This is not a system you want to be held to. We have the option of allowing these kinds of social structures to dominate us, or we can reject them. Yes, this is actually an extremely common form of worth-measuring in Western cultures. Your results speak for themselves and justify whatever your actions are. In a nutshell, winning dictates truth.

If you get great results from your fitness activity and that’s palpable to the people in your circle of influence, it must be right/worthwhile/good/true. But what happens when your results aren’t quite as good? When you get an injury or have to take time off? Who are you? The indicators are gone. The old gym swag you wore is out of fashion and now makes you stand out in the wrong way. Your kipping pull-ups look more like a fish out of water than an athlete setting a new PR. The people you used to do the activity with have moved away or now go to that new hip facility you don’t even know about. Where is your identity now?

Okay, okay, maybe this is blown out of proportion for many if not most people who exercise. You may not feel like your identity is indeed dictated by your healthy activities and community associated with them. However, the above rule reigns in more than just the fitness kingdom. It is alive and well in virtually every career setting. Let’s make a quick modification to apply to your career success: If your identity is decided by your actions as a professional, your worth is measured by your professional results. “You’re only as good as your last project.” “The proof is in the numbers.” The career world is results-based and has plenty of phrases to summarize that. As it should be. However, your worth, your value, your intrinsic ability to be known and loved and accepted is not results-based. Succumbing to the rule that you are only worth what you can produce is limiting who you are and what you are capable of. You are not a machine designed to meet output projections. At work or in a gym.

Know that whatever you choose to do, however, you leverage your limited resources, you are not the sum of the results you realize. Your life is not one large return on investment calculation. Be the best yogi, crossfitter, dancer, climber, manager, accountant, nurse practitioner, or retail clerk you can be all the while knowing that any label is just representing something you do, it’s not even close to describing who you are.

In the pursuit of any goal, you have to be tenacious to expect progress. Fitness, health, lifestyle changes are all no different. Except where they are.

Chances are good that we all have made more unhealthy choices than healthy ones. We grew up scavenging for candy like starving vultures. Circling the candy dishes, sneaking an extra piece or two and rushing off to devour our most recent kill. We likely begged the adults in our lives to allow us another scoop of ice cream, a milkshake with lunch, a handful of their french fries, or a super mega size sugary fountain drink.

We continue into adulthood with the inclinations intact. We tell ourselves things like, “Gosh, work was tiring this week. Maybe I’ll just indulge a little, not exercise yet, and make some yummy cookies!” We are fully grown people dang-it. We can do whatever we want. If that means eating a bowl of cookie dough while finishing the last 8 episodes of that show we sort of like but can’t stop watching, that’s what we are going to do. Period. You can’t stop me.

So if and when the point comes when we need to decide to turn our health in a positive direction, we have to battle these old ways. To battle anything, you must be fierce. You must not surrender. You must win!

Right?

Maaaaybe not. In my experience, with health-motivated actions anyway, this can actually be a great formula for failure, burnout, and resentment. The problem is we are but human. We DO get tired. We DO get busy with that home renovation project, that big work assignment, those sick kids, etc… And that interrupts our well-crafted plans to become fitness ninjas. So what do we have left as a course of action? Forget all about our plans? Forget all about our other life obligations and be muscly yoga hermits? Neither.

I suggest you have clear, achievable effort-based goals and/or attendance goals that are not easily shaken by other life events. Stating that you will do some kind of Pilates twice a week and cardio once a week is not as sexy sounding as “becoming a size 2” or “having a ripped six pack”. But there is a major difference between the 2 goals. One is based on factors you can control and the other is not. You can decide to participate in an activity which makes a positive impact on your health. You cannot force your stomach to become a particular geometric shape, especially one that looks like an ice cube tray.

Think about that for a minute.

Can you BY SHEER FORCE OF WILL tone your butt? No. You can’t. You can put in the work that “should” make that happen, but in the end, you cannot force results.

In a significant way, we are like farmers. Our bodies are the soil and our efforts are seeds. Our only true course of action is to exert effort in the way we best know how and wait for results. Plant those squats, water with lean protein and rest, and hope a booty will grow.

Don’t settle for lack of activity, for unhealthy diet habits, for a slothful life. Also, don’t settle for an all–or–nothing mentality. Both will fail you. Instead, realize that you will need to adjust your efforts to conform to the other circumstances in your life. Make it to the gym 3 times this week even if you only run on the treadmill for 9 minutes each time. You made it. Then next week when things aren’t on fire, get back to work on your regular routine. You will net the most results over the long haul by showing up and doing something. So do it.

Lately there has been a massive uptick in the popularity of “passive income” related content and strategies. Of course the concept is intriguing but it should be met with healthy amounts of questions and skepticism.

If passive income is so easy, why don’t more people take advantage of it?

If we can “make money while you sleep”, shouldn’t everyone be doing this?

How realistic are the claims being made by these smooth talking, promise-slinging geniuses of all things money?

Is this the way rich people became rich?

If you pay attention and listen between the alluring and ever-hopeful promises of the passive income gurus you may begin to realize that this income isn’t quite as passive as the name implies. Generally people either need large sums of money to generate regular income and/or it takes additional work to generate this income. So…not really passive at all. Quite active actually.

Earning the money needed to investment is active. And a side job called “real estate rental property” is far from passive. Other options include selling a product online, making an online course, selling stock photography, affiliate marketing, YouTube ad revenue, peer to peer lending, vending machines, drop shipping, renting items you already own, crowdfunded real estate, and the list goes on. Do you see the common theme? Startup money + hard work= the possibility of income. To me, that’s just the bones of starting a business.

Startup money + hard work= the possibility of income. To me, that’s just the bones of starting a business.

-truth hurts

So what is actually passive?

If income is to be TRULY passive it needs to require ZERO time or effort on your part. If you want to input extra time to monitor your progress or contribute work to potentially add value, that’s optional. In my mind the best and most passive sources of income have to be from the stock market.

The stock market is a complex, moody beast of a thing but we can choose to make it more or less so. Indexed funds allow us to invest in a low cost and automatically well diversified group of companies or funds without having to get an MBA or understanding a business prospectus statement. But there are people who still love to pick their own stocks and insist they are successful at choosing the ones that net them great passive income.

The experiment:

So to save you the headache and to satisfy my own curiosity I am going to invest in both ways: indexed funds and individual stocks. Not only that, I am choosing to invest specifically in companies and funds that have a track record of paying regular dividends to their investors.

Dividends are a portion of the profit made by the company that they choose to send to their investors. Generally companies that choose to pay dividends make this a regular occurrence. The most common schedule is quarterly payments, but that can vary wildly.

People like to recommend their own way of thinking when it comes to picking “good” stocks. They decide by reading about the company, looking at financial statements, mimicking other investors, or my personal “favorite”: if you “know the product and like it”. PLEASE read into the sarcasm here. That’s my “favorite” strategy because its so completely silly. Whether or not a company makes a product you personally like as 1 lowly consumer really has ZERO bearing on whether it’s a worthwhile investment. (Yes Apple, Tesla, Netflix, Facebook, and others have skyrocketed in value. And yes if you’d invested in them early on that would have been great. But for those of us who are getting started investing and don’t want the kind of risk associated with one stock rising and falling in value, there are other options)

In contrast to this method of choosing companies 1-by-1 I will also be investing in a number of funds that are a massive variety of companies that have a great record of paying their investors regular dividends. The benefit of these kinds of funds over a single company is that they are spreading your money over dozens or hundreds of companies. So if a few losers don’t pay a dividend this quarter, have a terrible year, or go out of business, it doesn’t hurt very badly. In contrast, if you’re expertly chosen gamble on that one company you think is “cool” happens to not work out, there goes your whole investment.

You can probably accomplish your entire goal of a relatively safe and good performing dividend investment with just 1 fund. However, in an effort to be as diverse as possible to prove the point, I will invest in several different funds full of dividend paying companies.

These 2 strategies will likely have some overlap since the handful of companies I pick will likely be included in the big funds in the other half of the investment experiment. So it’s not meant to single them out as good or bad or to judge my ability to pick a winner. It’s more to show the possible swings in performance and risk you accept when picking a small number of companies vs letting a fund do that work for you.

The 2 $1000 bets:

To complete this experiment I am using $2000 total. $1000 will go into the handful of individual stocks that are picked based on popular opinion and their track record for paying dividends reliably in the past. The other $1000 will be invested in a small number of dividend index funds. That’s it. They get to sit and stew and we will watch the rise and fall of their value as well as the actual amount of “passive income” that is generated by each account.

Contender #1: Robinhood

For the individual stock account I am using Robinhood. It is a tremendously popular app for people to use when getting started investing and is geared toward picking individual stocks and monitoring them closely.

You now have a claim to a stock like Apple, Ford, or Facebook. In order to keep this claim to your stock, sign up and join Robinhood using my link.

For the diversified index funds of companies I am using Webull. Webull is not nearly as popular as Robinhood but gives the user a TON of information about their investments. Far more than I ever want or need. But it’s impressive and if you’re wanting that kind of depth in your investment monitoring, Webull is the app for you. It also has a browser-based dashboard that shows a wealth of live updating detail and is guaranteed to help you feel like a stock broker in a movie scene!

Get 2 free stocks when you open and fund your account with Webull through my link:

Stay tuned for updates as the dividends roll in! I will post the breakdown of companies and funds as well as the exact dividends they paid!

Disclaimer: I am not a certified financial planner and hold no formal education or training in the field of investing or personal finances. Any and all information on this site is for entertainment purposes only and is not necessarily applicable to the reader’s personal situation and circumstances.

How can you advance your career in a matter of weeks or months with a mindset change? Especially if you’re a millennial like me? I’ll share my shameful but effective learning process with you to save you the time and trouble!

No this isn’t some silly fru-fru “I believe I can fly” positive self reinforcement B.S. But your mindset is very important and plays a major role in how you progress in your career and how successful you are in general.

I’ve recently experienced a massive shift in my mentality around work and motivation and it’s made a huge impact on my success therein.

My story: I’m in my early 30’s and have been working in the construction management industry for about 8 years. Before that I spent a few years in a retail management position and before that dabbled in sales. I’ve never been terribly successful professionally, until recently when I made this shift in my mentality.

I grew up as one of those kids who is naturally inclined at most things. Good grades, excelling at sports, making friends, etc… all came without much struggle. Being a millennial, whatever proficiency I displayed was always reinforced by participation ribbons, pats on the back and encouraging words. PLUS I grew up in a small town, so there was less competition. I was the “Valedictorian” of my junior high class of 27 students. Not a major accomplishment compared to a normal sized school!

To be honest I never thought about the incessant positive reinforcement we all got growing up but it inevitably shaped the way I thought. That environment reinforced the belief in myself that (you may also share) “you SHOULD be successful at the things you do”…basically always. But that expectation has a very limited lifetime and once you enter the real world of a career, it comes crashing down.

So as I entered the workforce it’s not that I wasn’t adding value or doing well, it’s that I was bringing less to the table that I thought I was. I was expecting a level of proficiency, and the associated rewards only reserved for those with levels of commitment and experience far greater than mine.

But that was a lesson I only learned through shame. Let me tell you that story:

A little over a year ago I got called into the boss’s office. I had been working on construction sites for the last 5 years, so getting an ambiguous meeting scheduled meant only 1 thing: promotion time! I had been doing a great job, was managing construction projects really well, no one had been seriously injured on my projects, they generally finished on time ( I even finished a project 2 weeks early!), and there could be no other real reason for a legitimate meeting except to formally announce that my career was going to the “next level”.

Orrrr so I thought.

I sat down with a smile, and readied myself for the big news. BUT instead of a shower of compliments and a new job title or bloated salary I got vaguely negative feedback. Something about how “I hadn’t arrived yet” and “wasn’t quite there”. Not that I had been doing a bad job, I was actually doing a good job, but it was definitely not “great”. It didn’t make sense to me….I zoned out trying to grasp what was happening….

Finally, the realization set in that this was going nowhere good. And even with clarifying questions I still didn’t really grasp where my performance wasn’t going well or how I could improve. In fact I began to get angry. Really angry. Not only did I not expect this but the least they could do is be direct! What does that even mean to “not arrive yet” or not quite be “there”?! Where the heck is “there”?

I reacted. Poorly.

I told my 2 bosses how hard I’d worked and how intentional I was. That my methods were probably the best way that the job could be done! I explained that this job wasn’t even a good fit for me. We’d talked about that in the past. About how it’s not very well suited to my strengths and they knew that. It was a blur. A frustrated, sweaty, tense, blur. I may have yelled. (Actually if you can’t remember whether or not you yelled, you probably yelled.)

I yelled.

This was a small office. Maybe 10’x15’. We were very close to each other. An arm’s length away. So my yelling was right in their faces.

To this day, to this very moment I can picture their surprised and disappointed facial expressions toward me. I can close my eyes and see them. Finally the meeting ended and I trudged out.

At the time the company needed building maintenance done so I was stuck doing manual labor for weeks afterward. Everyday I climbed up ladders and did roofing repairs. First, sweeping and pressure washing to clean them, then patching obvious holes, repairing and reattaching metal parapet cap material, then finally re-coating the entire roof surface before moving onto the next building and repeating the process. Alone with my thoughts… chewing…grinding…writhing alone on those rooftops with the boss’s feedback swirling around in my head. FURIOUSLY replaying those conversations in my head. Thinking about all the things I could have said. All the rebuttals I should have made.

Resentful roofing face

While roofing, I was passing the time listening to audiobooks. (Using the free Libby app through the public library system, which is awesome by the way) Business books, leadership books, entrepreneurial books, autobiographies of successful people, etc…. Hearing these people tell stories of overcoming their surroundings, becoming masters of their industries and fighting to succeed all started to sink into me.

What made them different from me?

Did they have “conversations” with their superiors like I did? Probably not.

What did they have that I lacked?

Somehow these successful people didn’t wait for their boss to give them some promotion or expect permission to advance. They just found a way. There was no rule book for the paths they took toward success and toward their goals! Obstacles didn’t stop them, they were mere speed bumps to navigate. If they had no contacts: they made contacts. If they didn’t know how to get a product made in a foreign country: they went out and discovered how. If they didn’t know how to sell their product: they worked tirelessly to get it placed in a major department store with untold amounts of creativity.

Basically they didn’t take their circumstances or their external factors of any kind as the final word. They had their goal and every morning they woke up and sprinted toward it no matter what.

Their goal. Their purpose. Their own source of motivation.

Why couldn’t I be driven like that? I had goals. I had a sense of who I was and the kind of person I wanted to be. What was I doing waiting around for someone else to give me what I wanted? Or to present me with the resolution to my goal or current obstacles? Whose fault was it that I was being held back and limited?

“No way!”, I thought. My goals won’t happen if I wait for someone else to make them happen. I need to go out and reel it in myself. I need to be the one to force this goal into existence whatever that means. (Obviously within the boundaries of what is legal and ethical but hey those are really huge and open boundaries) The company I work for and the people there can’t be the thing that I am waiting on to help me and I can’t allow them to slow me down either. The challenges in my work don’t have to be terminal or even huge. I can choose to mow them down one at a time and not look back.

Once that realization hit me fully, I knew I had to take action.

Ultimately this self motivation I was finally discovering had other names that I didn’t like and wasn’t happy with: Accountability. Ownership. Obedience. Discipline. These felt stodgy and limiting before but I had to come to terms with the FACT that they were the only means I had to overcome my doubts and my excuses.

I am accountable for my own success. I am the owner of it. I am the only person who has to make it happen. No one else has that on their radar and they shouldn’t. I am the person responsible for my own future and the discipline it takes to make it a good one.

It was like a door that was locked suddenly swung open. I was unleashed. Okay that sounds cheesy. But seriously, my whole perspective on life literally was changed from that time forward.

Solitude given a dirty roof

After this crazy realization and many roof repairs, I had another opportunity to work more closely with those same bosses that witnessed my feedback tantrum. But because my motivation had shifted so strongly from external factors (like them) to internal factors (like my identity as a highly capable and focused individual) I just put my head down and worked. It was fast, focused, and accurate work. I didn’t care about anything but getting the work done and learning like crazy.

Lets just say they noticed. Big time. They didn’t know “what happened to me” but wanted more of it. (Notice that language even falls into the commonly held belief that “something must have happened” to me like a terminal illness or I suddenly had to support a child etc…an external circumstance forcing a change on me.)

You can make a similar change and tap into a spring of motivation that was otherwise unused! Here’s how:

First you have to stop believing in extrinsic motivation.

Extrinsic Defined: “not part of the essential nature of someone or something; coming or operating from outside”

We blame someone else for not keeping us engaged and motivated. We blame our circumstances for holding us back. We blame our bosses for not recognizing the time and effort we put in. But then we stay in that cage we’ve made out of excuses. We act paralyzed because of those things, not realizing we have the power to create change for ourselves.

You never will have enough extrinsic motivation. Your tank is always only ¼ full and it can only be filled by factors outside of you.

Next we have to change our fuel source from extrinsic to intrinsic. Intrinsic motivation is different because it lives within you and feeds on the stuff YOU give it. It has less and less to do with other people.

You decide what drives you based on your own goals, metrics, and qualities of character.

You decide WHO do you want to be? You are “this kind of person” so you’re driven and motivated in these ways. It’s woven into your identity and is inseparable from your actions.

Example, “I am a hard working person who is driven to be successful and to bring excellence every day.” Now it’s personal. It’s reflective of who you are as a human being. You want to work hard on that project because it is just in your DNA to work hard. To be committed. To take its outcome personally. Yes you don’t know exactly how to do what needs to be done and that’s scary, but “afraid” isn’t in your core identity. The point is, you are staying true to your own integrity who you are choosing to be and what you care about. The only natural result of that is to live in line with that “new” identity. Be that person.

This is exactly the change that happened in me. Unfortunately for me the catalyst was negative feedback and the shame of my horrific reaction ruminated during weeks of manual labor on rooftops….

I want you to be able to recognize this in you now and change it.

Here’s an easy test: If you’re waiting on anything or anyone to become successful…you’re extrinsically motivated. (at least somewhat)

-Me

Here are more qualities of extrinsic motivations:

Focused on your effort

Waiting on someone or something to happen to allow you to be successful

Excuses outside your own choices

Circumstances are responsible for allowing you to progress or holding you down

You aren’t accountable

When you don’t know how to do something you Stop

Before committing you ask: What am I going to get out of this?

More examples of intrinsic motivations:

Focused on your results

Are only held back by your own drive or limits, no one else

You don’t believe in excuses

Circumstances come and go but you keep moving forward

You are accountable

You learn what it takes to continue and don’t stop

Before starting you ask yourself: What value am I bringing to this?

My challenge to you is to sit down for a few minutes and really be honest with yourself.

Where are you?

Are you in the extrinsic camp or the intrinsic camp?

What do you allow to slow yourself down?

What obstacles have you accepted as terminal?

Who are you waiting on to give you the golden ticket to success? If it has been of any value please send it to someone you know who it could also help.

SO many little quips revolve around saving money. I feel like the implication is that they somehow summarize everything you need to know to handle your money well.

But that’s bogus! Money is complicated. Or at least our lives are complicated so the way we choose to deploy our money is also complicated. That’s why I think we need to think with a little more nuance about what saving our money is for and what it can never accomplish.

FIRST: Why saving money is great essential! And a little childish…

Spending everything we make (or more) is a losing proposition. We can never catch up, pay off debt, create a secure financial footing, build wealth, or hope to have the option of retiring from full time work. If that’s the place you’re currently in: no shame and no blame. Not from me, not from yourself, not from anyone else on the internet. Yes it’s an objectively bad habit to be in but shame/blame/built aren’t going to help change things.

So we are left with the next logical step which is to save some portion of our income. I.E. intentionally spending less than we make so we can set it aside. Wisdom. Delayed gratification. All that jazz. But hearing things like “pay yourself first” honestly has only served to cloud my mind in years past. What the heck is that supposed to mean!? (I finally learned that it is just a cryptic way of saying you should save some money before you start spending it on non-essential items)

I used to save money in a wooden and plexiglass kids bank shaped like a dog. His belly was see-through since it was made of plexiglass and you could see the little coins and bills piling up over time. To access them you had to literally disassemble the thing with 9 tiny screws. But that’s what I did countless times! I couldn’t wait to let the money pile up. Having to count it over and over I’d grab a tiny screwdriver and take it apart to get my new total. Then it would get carefully reassembled and put back on the shelf.

Stashing some money in cash or even in a savings account is really not much different than my childish activities 25+ years ago. We know it’s the right thing to do and put some money off to the side. It has no real intent or purpose, but its there and we are doing what we’ve been told is the “right thing”. The problem is that we don’t have much of a grasp on what’s happening overall, which doesn’t allow for intention to be baked into that savings, which limits its power to help us.

We need a general game plan. I’d summarize that as: have an accurate budget, have a plan for debt repayment, and have a plan to grow your wealth. Saving money needs to have a direction into 1 of these 3 buckets or it will be stuck in that aimless, child-like state like my doggy-bank dollars.

SECOND: Saving is a foundation. But only a foundation

Assuming we have a budget, a plan for debt, and a solid vision for a wealth-building future do we just save as hard as possible? Yes and No.

Saving is the first step in the process of wealth building. We have to hang onto money and not let it fly out the door to subscriptions and restaurants and nasty bills. It is the only way we can stop the cycle of living paycheck to paycheck.

We all need a small chunk of money that is a basic buffer while money flows in and out of our accounts so as to avoid bouncing a payment. This can be as little as a few hundred dollars or as much as a few thousand depending on your comfort level, when bills are paid, and how big those bills are. If you want a good buffer, have everything set on autopsy for the 1st of the month and spend a lot on recurring bills you may need $3000-$6000 as a buffer. But if you’re ok with a tighter budget, have bills spread out across the month, and don’t have many large expenses you could probably get away with $500-1000 quite comfortably.

After a buffer, everyone needs an emergency fund. Actually your buffer is the start of your emergency fund because it’s the bare minimum in whatever account(s) you use. In a real emergency it’s likely the money that gets spent first. But over and above this an emergency fund should be set aside in it’s own account, distinctly earmarked for emergencies only. “Emergency” means unpredictable, accidental, or otherwise out of your control. If it IS in your control or can be foreseen that falls into the next category of “sinking funds” but more on that in a minute.

An emergency fund is directly proportional to 2 elements. 1: What comfort level are we after? 2: What are our average monthly expenses? For number 1, this is literally a matter of preference. Part of that preference has to do with how regular income is for the household. The more variable the income, the larger the emergency fund should be. However, most people outside of commision-only jobs are paid fairly regularly. Number 2 is important because the amount of emergency funds we need to set aside depends on how fast it will be used. If you’re a high income/high spending household that’s much different than a single student living at home.

Rules of thumb for emergency funds: Always have at least 1 month of living expenses. Set a baseline goal after that of 3 months worth of living expenses. If your income is wildly variable, bump that baseline goal to 6 months or equal to the average span of your sales/paychecks. Any more than these amounts and you’re probably giving up a lot of wealth-producing potential! Unless you’re saving for a specific upcoming need: a sinking fund.

Third: Saving for a “sinking fund” (aka rainy day)

This area of saving stands to lift the most people out of the evil clutches of consumer debt and I to the glorious paradise of freedom: saving for big purchases. Wait! Stay with me! Don’t turn away because you just threw up in your mouth a little bit like I did thinking about this particular topic! I know it’s repulsive or at least horrifically boring to slowly and methodically save for a premeditated purchase months or years in advance. I get it. But we have to do something new to get a new result.

We have to do something new to get a new result.

-Me…again

If you bought a house and expect the air conditioner to kick the bucket in the near-ish future but don’t save for it, that’s just silly. (This is what my wife and I did by the way, we bought that house. 3 years in and the old thing is still somehow functioning!) Or if the current vehicle is steadily creating more and more bills from the mechanic shop we have to acknowledge that reality with a plan. And plans often take time to come to fruition.

We are responsible for our financial futures so it’s our responsibility to forecast the big expenditures. Making a quick list in a phone app or notepad with the impending biggies for the next 1-3 years can add huge amounts of perspective. With it, we are better able to act in the present. “Can we afford to go on that 2 week cruise” becomes easier to answer if Christmas is around the corner along with a new washing machine.

Keep your list handy and update it often. It’s easy math to figure out how long it will take to save for an upcoming purchase. (The math is easy. The saving is harder!) Let’s say an expense is coming up in about 5 months. It is going to cost around $900. $900/5= $180, so every month from now until the big purchase we need to set aside $180 and not touch it! That can be the hardest part, seeing the funds accumulate and leaving them alone, destined to fulfill their true purpose.